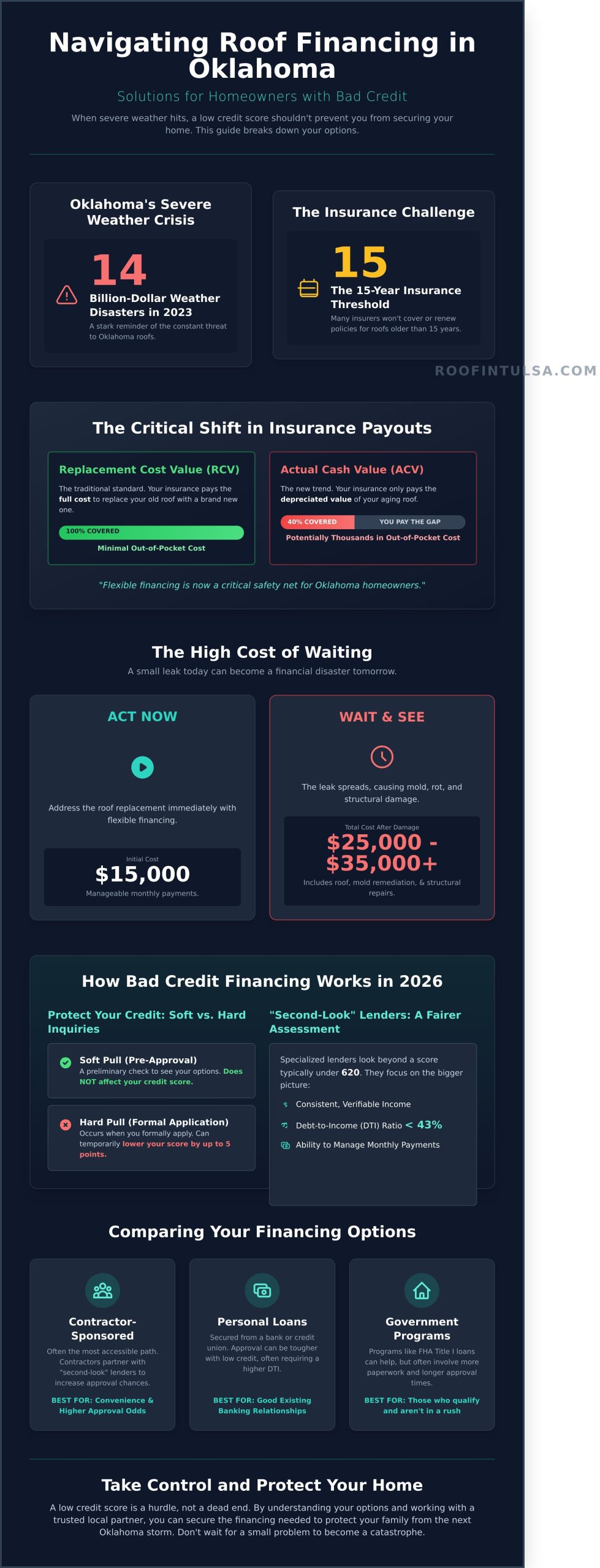

In 2023, Oklahoma was battered by 14 separate billion-dollar weather disasters, a stark reminder of how critical a sound roof is for every local family. When you’re facing another Tulsa storm season with a damaged roof, a low credit score can feel like a closed door, trapping you in a cycle of anxiety over worsening leaks and denied insurance claims. We understand that stress. You need a safe home, not another financial rejection that dings your credit further.

This guide was built to give you honest, local solutions. We promise to show you that securing quality roof financing for bad credit in Oklahoma isn’t just possible; it’s achievable without the hassle you’re expecting. We’ll walk you through trusted local financing pathways designed for real Oklahomans, share proven strategies for maximizing your insurance claim, and help you find a durable new roof with a monthly payment that brings you peace of mind. It’s time to protect your home and family, regardless of what a credit report says.

Key Takeaways

- Learn the key differences between contractor-sponsored financing, personal loans, and government programs to find the best fit for your situation.

- Understand how specialized “second-look” lenders are making roof financing for bad credit oklahoma more accessible than ever, even with a low score.

- Discover the crucial difference between “soft” and “hard” credit inquiries so you can explore your options without damaging your credit.

- Follow a clear, step-by-step strategy to gather the right documents and prepare a strong application for the highest chance of approval.

The Reality of Roofing in Oklahoma with Credit Challenges

Living in Oklahoma means you understand the weather is unpredictable and often unforgiving. Hail, high winds, and the constant threat of tornadoes put immense stress on the most critical part of your home: its roof. When that roof needs urgent replacement, the last thing you want to worry about is your credit score. We’re here to help you understand that a less-than-perfect credit history doesn’t have to stand between your family and a safe, secure home.

Roof financing for bad credit is a specialized type of loan designed for homeowners with credit scores typically under 620. For many Oklahomans working on understanding your credit score and its impact, seeing that number can feel like a closed door. But it’s not. It simply means you need a trusted, local partner who works with lenders that look beyond the score to see the person and the need. Your family’s safety should never be compromised by a past financial challenge.

Why Oklahoma Roofs Are Getting Harder to Insure

The ground is shifting for Oklahoma homeowners. Many insurance carriers are tightening their policies, making it tougher to get a damaged roof fully covered. A major challenge, especially in the Tulsa area, is the “15-year insurance threshold,” where many companies will refuse to renew a policy or cover a replacement on a roof older than 15 years, no matter its condition. This policy puts a ticking clock on your home’s protection. Adding to this pressure are significant policy changes taking effect statewide.

- Replacement Cost Value (RCV): This was the standard. It paid the full amount to replace your old, damaged roof with a brand new one.

- Actual Cash Value (ACV): This is the new trend. ACV policies only pay for the depreciated value of your existing roof, leaving you to cover the gap, which can be thousands of dollars.

“In 2026, Oklahoma homeowners are increasingly finding that insurance covers less, making flexible financing a critical safety net.”

The High Cost of Waiting: Why “Later” is More Expensive

Putting off a roof replacement is a gamble you can’t afford to take in our climate. A small, seemingly minor leak from a hail-damaged shingle doesn’t stay small. With Tulsa’s humidity, that moisture seeps into your attic’s insulation, promotes toxic mold growth, and begins to rot the wooden decking and structural supports of your home. Suddenly, a roof problem becomes a whole-house disaster.

Consider the financial reality. A new roof might cost $15,000, which is a manageable monthly payment with the right financing. Waiting could lead to that same roof replacement plus an additional $10,000 to $20,000 in mold remediation, insulation replacement, and interior drywall repair. The emotional cost is just as high. Every time the storm sirens go off, you shouldn’t have to feel a wave of “storm anxiety,” worrying if this is the storm that turns a small issue into a catastrophe. Securing reliable roof financing for bad credit oklahoma provides more than just shingles; it provides peace of mind.

How Roof Financing for Bad Credit Works in 2026

Finding a new roof loan with a damaged credit history can feel overwhelming, but the process in 2026 is more flexible than you might think. Many modern lenders now look beyond a simple three-digit credit score. They focus on your overall financial stability to determine eligibility, giving Oklahoma homeowners a fair chance to protect their homes.

The first step is understanding the difference between credit inquiries. A “hard pull” happens when you formally apply for a loan. This action is reported to credit bureaus and can temporarily lower your score by up to five points. A “soft pull,” on the other hand, is a preliminary check that does not affect your credit score at all. Reputable roofing partners will always start with a soft pull to see what you qualify for without any risk.

This is where specialized “second-look” lenders come in. These financial institutions partner with contractors to provide roof financing for bad credit oklahoma residents. Instead of automatically declining applications with scores below 640, they prioritize factors like consistent income and your ability to manage monthly payments. They are looking at the whole picture, not just past mistakes.

For Tulsa residents, in particular, lenders place significant emphasis on your debt-to-income (DTI) ratio. This metric compares your total monthly debt payments (like car loans and credit cards) to your gross monthly income. A DTI below 43% demonstrates that you can comfortably afford a new loan payment, often outweighing a lower credit score in the lender’s decision.

Soft-Pull Pre-Approval: Protecting Your Score

A soft-pull pre-approval allows you to check your eligibility for financing with zero impact on your credit score. You simply provide basic information like your name, address, and estimated income. This process is designed to give you options without risk. It’s vital to distinguish between legitimate partners and predatory lenders who might demand high upfront fees or use pressure tactics. A great way to protect yourself is by becoming familiar with fair lending practices and understanding your home loan options through trusted resources like the Consumer Financial Protection Bureau (CFPB).

The Role of Co-Signers and Joint Applications

If your credit score is below 550, a co-signer can be a powerful asset for securing a loan. A co-signer, often a spouse or trusted family member with a strong credit history, agrees to take on full legal and financial responsibility for the loan if you are unable to make payments. Their good credit history provides the lender with the security needed for approval. It’s a serious commitment that requires trust and open communication. Our team can help you explore every safe option to find the best path forward for your family.

When considering a co-signer, use this simple checklist:

- A Trusted Relationship: The person should be a spouse, parent, or family member with whom you have complete trust.

- Financial Stability: They need a stable, verifiable income and a credit score of 670 or higher.

- Clear Understanding: Ensure they fully understand they are 100% responsible for the debt if you default.

Comparing Your Options: Which Financing Path is Right?

When your roof is failing, choosing how to pay for it can feel as overwhelming as the repair itself. Don’t worry. You have several solid paths forward, and understanding them is the first step toward peace of mind. We’ll break down the most common options available to Oklahoma homeowners, from fast contractor financing to government-backed programs, so you can make a confident, informed decision for your family.

The core decision often comes down to weighing the immediate cost of a loan against the long-term cost of delaying repairs. A leaking roof doesn’t wait. A small leak today can lead to thousands in structural damage, attic insulation replacement, and mold remediation within 6 to 12 months. While a bad credit loan might have an APR between 15% and 25%, that cost is often significantly less than the $5,000 or more you could spend on secondary repairs if you wait. Securing financing protects your home’s value and prevents a small problem from becoming a catastrophe.

Contractor Financing vs. Traditional Bank Loans

For homeowners needing a new roof quickly, contractor-sponsored financing offers a distinct advantage over a traditional bank or home equity loan. The biggest difference is speed. Our lending partners can often provide an approval decision in minutes, not weeks. A typical bank loan can involve a 30 to 60-day underwriting process, a delay you simply can’t afford with an active leak. Because our lending partners specialize in home improvement, they have more flexible credit requirements and higher approval rates for scores that banks might decline. This streamlined approach provides a truly hassle-free experience; we handle the integration, so your financing and installation are managed under one roof, with one trusted point of contact.

Government and Regional Assistance in Oklahoma

Several federal and local programs are designed to help Oklahomans protect their homes. FHA Title I loans, for example, are insured by the government and can be used for home improvements up to $25,000. These are often accessible to homeowners with less-than-perfect credit or limited home equity. For major projects where a roof replacement is part of a larger structural renovation, an FHA 203(k) Rehabilitation Loan might be the right fit.

It’s also worth exploring assistance right here in our community. For Oklahomans in rural areas, the USDA Section 504 Home Repair Program provides loans and grants to help very-low-income homeowners repair and modernize their homes. Additionally, cities like Tulsa sometimes offer funds through Community Development Block Grants (CDBGs) for essential home repairs. This is the power of local expertise. As an Oklahoma-based roofer, we understand the regional programs and lenders who are invested in our communities. They see you as a neighbor, not just a credit score, which is essential when seeking roof financing for bad credit in Oklahoma.

Ultimately, the best path is the one that gets your family under a safe, reliable roof without delay. Working with an experienced local contractor gives you access to a network of pre-vetted lenders who want to say “yes.” We do the hard work of finding the right financing partner so you can focus on protecting your home.

A Step-by-Step Strategy for Tulsa Homeowners

Feeling overwhelmed by the need for a new roof when your credit isn’t perfect is completely understandable. But you have a clear path forward. We believe in providing honest guidance, not just quality roofing. This simple, four-step strategy can dramatically increase your chances of getting approved for the roof financing you need, right here in Tulsa.

Follow these steps to take control of the process and secure protection for your home:

- Get a Professional, Free Inspection. Before you can apply for anything, you need an exact number. A detailed, professional inspection from a trusted local roofer provides the precise project scope and cost. This isn’t a guess; it’s the official quote you’ll use for your application, preventing you from asking for too little or too much.

- Gather Your Key Documents. Lenders need to verify three things: your income, your Oklahoma residency, and that you own the home. Having these documents ready shows you’re serious and prepared. Typically, you’ll need your last two pay stubs, a recent utility bill, and your property deed or a recent mortgage statement.

- Attempt a Soft-Pull Pre-Qualification. Don’t start applying everywhere. A “hard inquiry” can lower your credit score by a few points. We partner with lenders who use a “soft pull” for pre-qualification, which has zero impact on your credit score. This allows you to see potential offers without any risk.

- Focus on the Monthly Payment. It’s easy to get fixated on the interest rate, but the monthly payment is what truly affects your budget. A slightly higher rate with a payment you can comfortably afford is a much better financial decision than a lower rate with a payment that strains your finances every month. Look for a plan that fits your life.

Preparing Your Financial Profile for Approval

Taking a few small actions in the 30 days before you apply can make a big difference. Try to pay down a small credit card balance; even reducing a card’s balance by $300 can lower your debt-to-income (DTI) ratio. Debt-to-income ratio is the percentage of your gross monthly income that goes toward paying debts. If you have derogatory marks, be prepared to discuss them honestly. A medical collection from two years ago is viewed very differently than a recent pattern of missed payments.

Navigating the Insurance Claim as a Financing Alternative

Before seeking roof financing for bad credit oklahoma, always explore your insurance options. We recommend starting with our “Hassle-Free” storm damage inspection. Our trained experts may identify wind or hail damage that qualifies for a full replacement through your homeowner’s policy. If your claim is approved, you may only need financing to cover your deductible, which Oklahoma law requires you to pay. This can turn a $15,000 problem into a much more manageable $1,000 or $2,500 one. For a complete walkthrough, see our Insurance Claim Assistance page.

You don’t have to navigate this alone. The first step is always understanding the true condition of your roof. Schedule your free, no-obligation inspection today and let our team provide you with an honest assessment and a clear plan of action.

Rescue Roofing Tulsa: Your Local Partner for Hassle-Free Financing

Navigating roofing issues is stressful enough without the added worry of a complicated financial process. At Rescue Roofing Tulsa, we aren’t a faceless national chain. We’re your neighbors. We live here, we work here, and we understand the unique challenges Oklahoma weather throws at our homes. That’s why we’ve built a support system, not just a roofing company, to help our community protect their most valuable asset. We believe every family deserves a safe roof, and we’ve created a process for roof financing for bad credit oklahoma residents that is built on trust and local understanding.

Our commitment to you goes far beyond a simple transaction. As a GAF Master Elite® Certified roofer, we belong to the top 2% of all roofing contractors in North America. This isn’t just a plaque on our wall; it’s your assurance of superior workmanship and long-term value. This certification allows us to offer the best warranties in the industry, like the GAF Golden Pledge® Limited Warranty, which covers both materials and our workmanship for decades. A roof from us isn’t just a repair; it’s a lasting investment in your home’s safety and value.

Why Our Financing is Different

We’ve streamlined our process to remove the typical barriers and anxieties homeowners face. Our approach is founded on three core principles that ensure you get the best possible outcome with complete peace of mind.

- Investment Protection: Your new roof is backed by our 10-year, ironclad workmanship warranty. This is our promise to you that the job is done right the first time, protecting your financial investment for a full decade.

- Honest and Transparent Pricing: You will never find hidden fees or surprise charges on our invoices. We provide detailed, line-item estimates and walk you through every cost, so you know exactly where your money is going before any work begins.

- Local Insurance Advocacy: We have years of experience working directly with Tulsa-area insurance adjusters. We know how to document damage properly and advocate on your behalf to help you maximize your claim, reducing the amount you need to finance.

Your New Roof Starts with a Conversation

Taking the first step is the easiest part. We don’t use high-pressure sales tactics because we believe our work and our reputation speak for themselves. Our goal is to provide you with a clear, honest assessment of your roof’s condition and a transparent overview of your financial options. We are confident we can find a solution that works for you. Your family’s safety is our priority, and we have the tools and partnerships to secure your home with a durable, high-quality roof, regardless of your credit history.

Don’t let financial worries prevent you from protecting your home. Let’s talk about your options today. It all starts with a simple, no-obligation inspection.

Get Your Free Tulsa Roof Inspection and Financing Quote

Take the Next Step Toward a Secure Oklahoma Roof

Protecting your home from Oklahoma’s weather is non-negotiable, even with credit challenges. This 2026 guide has shown that a less-than-perfect score doesn’t have to be a barrier to a safe roof. The key is understanding that options exist and that a strategic approach makes all the difference. Navigating the world of roof financing for bad credit oklahoma is much simpler with an experienced, local partner by your side. At Rescue Roofing Tulsa, we believe every family deserves peace of mind.

As Tulsa’s Most Trusted Local Roofer and a GAF Master Elite Certified contractor, we’re committed to finding a solution that works for you. Every roof we install is backed by our 10-Year Workmanship Warranty. Don’t wait for a small leak to become a major problem. Your path to a safe, durable roof is clearer than you think.

Secure Your Home with Hassle-Free Financing Today and let our trusted team help you get started.

Frequently Asked Questions About Roof Financing

Can I get roof financing in Oklahoma with a 500 credit score?

Yes, getting approved for roof financing with a 500 credit score is possible. We partner with specialized lenders who look beyond just the credit score, considering factors like income and home equity. While interest rates may be higher, typically between 15% and 25%, these programs are designed to help homeowners protect their most important asset. We can guide you through the application to find the best possible terms.

Do roofing companies in Tulsa offer monthly payment plans?

Absolutely. Reputable Tulsa roofers, including our team, provide flexible monthly payment plans to make your new roof affordable. We work with trusted financing partners like Service Finance and GreenSky to offer a variety of options. These plans often feature terms ranging from 12 to 60 months, allowing you to choose a payment that fits comfortably within your family’s budget without delay.

How much does a new roof cost in Oklahoma for a standard home?

For a standard 2,000-square-foot home in Oklahoma, a new asphalt shingle roof typically costs between $8,000 and $12,500. The final price depends on specific factors like the type of shingle you choose (e.g., 30-year architectural vs. standard 3-tab), the steepness of your roof, and the complexity of the job. A free, honest inspection from our team will give you a precise, no-obligation quote.

Is it possible to finance a roof deductible in Oklahoma?

Yes, you can finance your insurance deductible. Many of our financing plans can be structured to cover the entire project cost, including your deductible amount, which is often between $1,000 and $2,500. This is a common solution that allows you to get a high-quality roof replacement started immediately after a storm, ensuring your home is protected without a large upfront cash payment. We make the process simple and hassle-free.

What is the “15-year rule” for roofs and insurance in Tulsa?

The “15-year rule” is a guideline used by many Oklahoma insurance carriers where they may reduce coverage on roofs older than 15 years. Instead of paying the full Replacement Cost Value (RCV), they may only cover the Actual Cash Value (ACV), which accounts for depreciation. This means if your 16-year-old roof is damaged, your payout could be 40-50% less, leaving you to cover the difference.

Will applying for roof financing hurt my credit score further?

Applying for financing will not significantly harm your credit. Most of our lending partners use a “soft inquiry” for pre-qualification, which has zero impact on your credit score. If you decide to accept an offer, a “hard inquiry” is placed, which might lower your score by less than 5 points temporarily. Making consistent, on-time payments will quickly build positive credit history and offset this minor dip.

Can I use a HELOC for a new roof if I have bad credit?

It can be very challenging to get a Home Equity Line of Credit (HELOC) with bad credit, as most banks require a minimum credit score of 680. Because a HELOC is secured by your home, lenders have strict approval criteria. Our dedicated options for roof financing for bad credit in Oklahoma are specifically designed for this situation and are often a much more accessible path to getting your new roof.

What happens if my roof financing application is denied?

If one application is denied, don’t lose hope. We’re here to help you explore other avenues. We work with several different lenders, and a denial from one doesn’t mean a denial from all. We can also discuss options like adding a qualified co-signer to your application or, in some cases, breaking the project into smaller, essential repairs that can be managed until a full replacement is feasible.