On June 18, 2023, a massive windstorm with gusts reaching 100 mph swept through Tulsa, leaving thousands of homeowners staring at damaged shingles and fallen limbs. If you’ve recently walked outside after a typical Oklahoma storm to find debris in your yard, you’re likely wondering how to file a roof damage insurance claim without getting overwhelmed. That sinking feeling in your stomach is completely understandable, especially when you’re worried about the safety of your family and the daunting task of dealing with insurance adjusters who seem to speak a different language.

We believe that restoring your home should be a source of relief, not extra stress. You shouldn’t have to navigate complex paperwork alone or fear a sudden claim denial. This guide provides the exact roadmap you need to secure an approved claim for a full roof replacement with minimal out-of-pocket costs. We’ve simplified the entire journey into a hassle-free, step-by-step process. We’ll cover everything from the initial professional damage assessment to the final installation of your new roof, giving you the peace of mind you deserve as a member of our Tulsa community.

Key Takeaways

- Learn the essential 5-step process to navigate the insurance landscape with confidence after a Tulsa storm.

- Discover exactly how to file a roof damage insurance claim to ensure you receive the full coverage your policy provides.

- Understand the critical difference between ACV and RCV payouts to avoid unexpected financial surprises during your roof replacement.

- Find out why having a professional contractor present during the adjuster’s inspection is your best defense against undervalued claims.

- See how Rescue Roofing Tulsa’s local expertise and Master Elite status provide a hassle-free path to protecting your home.

Understanding Roof Damage Coverage in Tulsa, Oklahoma

Tulsa weather is notoriously unpredictable. You might wake up to a clear sky and end the day dealing with a severe thunderstorm or a sudden supercell. For Green Country homeowners, the roof is the first line of defense against these elements. Knowing how to file a roof damage insurance claim begins with a clear look at your specific policy. Most Oklahoma homeowners insurance policies cover “perils,” which are specific events that cause physical damage to the structure.

Understanding Property Insurance is the best way to see how “Replacement Cost Value” differs from “Actual Cash Value.” If your roof is older than 15 years, your payout might be lower based on depreciation. Whether you have standard asphalt shingles or a durable metal roof, the type of material also dictates how an adjuster assesses the damage. It’s vital to remember that insurance is not a maintenance plan. It covers sudden, accidental damage rather than long-term wear and tear or neglect.

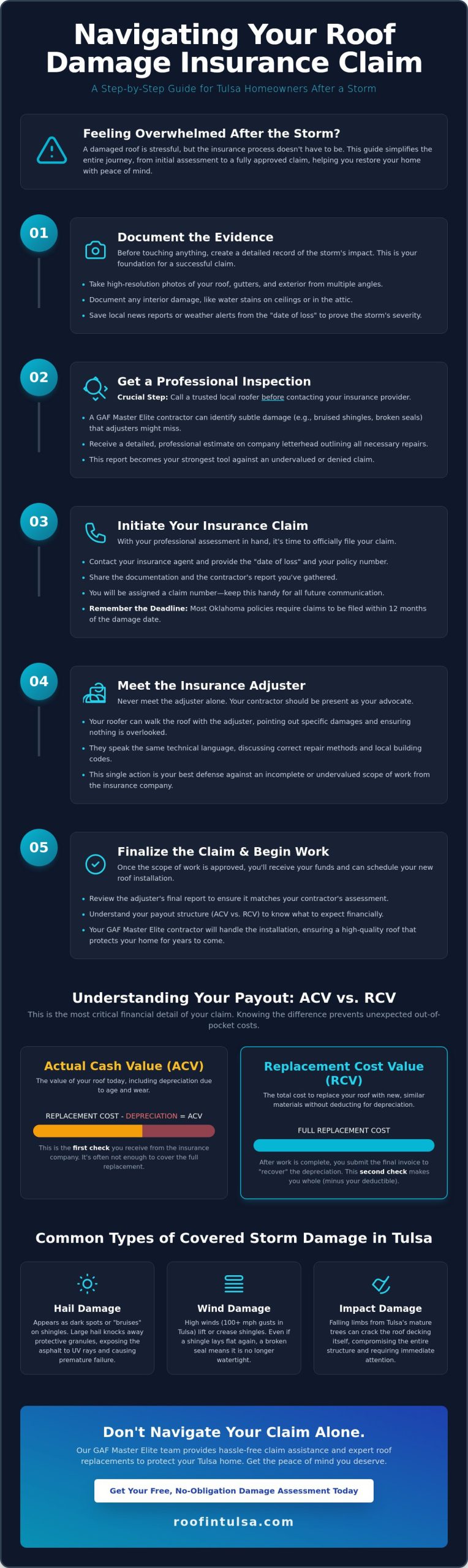

Common Types of Covered Storm Damage

- Hail damage: This often appears as dark spots or “bruises” on shingles. Large hail can knock away protective granules, exposing the asphalt underneath to harmful UV rays and leading to leaks.

- Wind damage: High winds can lift shingles or create “creased tabs” where the shingle has folded back. Even if the shingle is still attached, a broken seal means your home is no longer watertight.

- Impact damage: Falling limbs from Tulsa’s mature oak and pecan trees can crack the roof decking. This requires immediate professional attention to prevent structural failure.

Tulsa Climate Factors and Your Policy

Tulsa’s location in Tornado Alley means we face some of the most intense weather in the country. Because of the high volume of claims after a major storm, insurance adjusters get busy quickly. You should act fast to ensure your home is protected and your claim is prioritized. If you are wondering how to file a roof damage insurance claim after a spring storm, the first step is identifying the exact date the damage happened.

The “date of loss” is the specific calendar day the storm hit your property, and it serves as the official starting point for your filing deadline. Most Oklahoma policies require you to report the damage within 12 months of this date to remain eligible for coverage. At T-Town Roofing, we’ve spent years helping neighbors navigate these complexities. We are GAF Master Elite contractors, which means we understand the technical side of storm damage. We’re here to provide a professional assessment so you can move forward with confidence and peace of mind.

5 Steps to File a Roof Damage Insurance Claim

Dealing with storm damage is overwhelming for any homeowner. Your first priority is always safety. Before you step outside, check for downed power lines or structural sagging. If you notice active leaks, use a tarp to prevent further interior damage. Most insurance policies actually require you to take these reasonable steps to mitigate loss. Once the immediate threat is handled, you can begin the process of restoring your home’s protection.

Step 1: Documenting the Evidence

Start your documentation before you move any debris or begin repairs. Take high-resolution photos of your roof, gutters, and your property’s exterior. In Tulsa, we often see hail larger than 1.75 inches during spring storms, which can leave subtle but serious impact marks. Save local news reports or weather alerts from the specific date of the storm. Don’t forget the inside of your home. If water is dripping into your attic or living room, document the damage to your ceiling and personal property. This creates a clear timeline for the claims department and provides proof of the event’s severity.

Step 2: The Professional Inspection

Before you call your insurance company, contact a local roofing contractor for a thorough assessment. Adjusters often have dozens of homes to visit after a storm and might miss subtle signs of damage. A professional roofer identifies issues like bruised shingle mats or compromised flashing that aren’t visible from the ground. You should receive a detailed repair or replacement estimate on company letterhead. It’s vital to understand that this estimate is a professional opinion of the work needed. It differs from the final claim payout, which the insurance company determines based on your specific policy limits and deductibles.

Once you have your contractor’s report, it’s time to contact your insurance agent to initiate the official claim. Provide them with your documentation and the professional estimate to get the ball rolling. Compiling a comprehensive package for the claims department makes the entire process more efficient and reduces the back-and-forth communication.

The final step involves coordinating the adjuster meeting. You should always have your contractor present during this inspection. They speak the same technical language as the adjuster and can point out specific areas of concern that were noted during the initial professional inspection. This ensures nothing is overlooked and helps you get a fair assessment. If you’re feeling stressed about the process, you can reach out to a local expert to help you navigate these steps with confidence.

Learning how to file a roof damage insurance claim is about being prepared and proactive. By following these steps, you protect your investment and ensure your Tulsa home stays dry and secure for years to come. Professional guidance makes the transition from storm damage to a full recovery much smoother.

Actual Cash Value (ACV) vs. Replacement Cost Value (RCV)

Understanding the financial side of your policy is a vital part of learning how to file a roof damage insurance claim. Most Tulsa homeowners carry one of two coverage types: Actual Cash Value (ACV) or Replacement Cost Value (RCV). The difference between these two determines how much money stays in your pocket after the project is finished.

ACV pays you for the current worth of your roof. If your shingles are 12 years old, the insurance company subtracts “depreciation” from your payout based on that age. You receive a smaller check because the materials have lost value over time. RCV is the preferred option for many. It covers the full cost to replace your roof with a brand-new one of similar quality, regardless of how old the original roof was. When you are learning how to file a roof damage insurance claim, these definitions help you set realistic expectations for your budget.

If you have an RCV policy, you’ll usually receive two separate payments. The first check is the ACV amount. The second check, known as “recoverable depreciation,” is sent after the work is finished. This two-step process ensures the insurance company only pays the full amount once they verify the new roof is installed. It’s important to note that many Oklahoma insurance providers are now shifting roofs older than 15 years to ACV-only schedules due to the high frequency of local storm cycles.

Calculating Your Out-of-Pocket Costs

Your deductible is the specific amount you must pay before insurance coverage kicks in. If your roof replacement costs $15,000 and your deductible is $2,000, the insurance company provides a total of $13,000. Under Oklahoma law, specifically House Bill 1944, it’s illegal for a contractor to waive or absorb your deductible. Any roofer offering to do this is committing insurance fraud and puts you at legal risk. You should also budget for upgrades. If you want to move from standard shingles to impact-resistant Class 4 shingles for better protection against Tulsa hail, you’ll typically pay that price difference yourself.

Common Insurance Terms to Know

Knowing these terms makes the process hassle-free and gives you peace of mind while talking to your adjuster:

- Supplementing: This is the process of adding missed items, such as rotted decking or extra flashing, to the claim after the work begins.

- Depreciation: This is the calculated loss of value based on the age and condition of your roof at the time of the storm.

- Letter of Completion: A Letter of Completion is a signed document that notifies your insurance company the project is finished so they can release your final payment.

At T-Town Roofing, we believe in being a trusted advisor for our neighbors. We provide the documentation your insurance company needs to process these checks quickly, ensuring your home is protected by a durable, high-quality roof.

How to Prepare for the Insurance Adjuster Meeting

Understanding how to file a roof damage insurance claim is only half the battle. The adjuster meeting is where your claim’s value is truly decided. An insurance adjuster’s role is to assess the damage on behalf of the insurance provider. While they are professionals, their primary goal is to document loss based on the company’s specific criteria. This is why you should never meet an adjuster without your roofing contractor present. Having a trusted expert by your side ensures that the inspection is thorough and fair.

Before the adjuster arrives, your contractor should have already completed a detailed inspection. We provide the adjuster with a professional damage report that includes high resolution photos and measurements. This report acts as a roadmap for the meeting. We guide the adjuster to specific areas of concern, ensuring they don’t overlook “soft metals.” In Tulsa, hail often leaves clear evidence on gutters, box vents, and flashing. These surfaces show impact marks more clearly than shingles, providing undeniable proof of the storm’s intensity.

The Benefit of Professional Advocacy

Contractors who understand the insurance industry speak a specific language. We use the same estimating software as most major carriers, which helps us compare line items accurately. After the meeting, we review the adjuster’s summary to ensure it includes everything required for a proper fix. It is common for initial summaries to miss essential components like ridge caps, starter strips, or drip edges. If the damage is limited to a small area, you may only need the roof repair Tulsa residents rely on for quick, reliable fixes. Our goal is to ensure your home is returned to its pre-storm condition without cutting corners.

What if Your Claim is Denied?

It is frustrating to receive a denial, but it isn’t always the final word. Claims are often denied due to “pre-existing wear” or a perceived lack of storm evidence. If you feel the assessment was inadequate, you have the right to request a second inspection. You can ask for a different adjuster or a supervisor to visit the property. In more complex cases, you may invoke the “appraisal clause” in your policy, which involves a neutral third-party umpire. Following the June 18, 2023, wind storm in Tulsa, many homeowners successfully overturned initial denials by providing more robust photographic evidence and contractor testimony. We stand by our customers through every step of this process to ensure they receive the coverage they pay for.

Don’t face the insurance company alone. Let our experienced team handle the details and advocate for your home. Contact Tulsa’s most trusted roofer today to schedule your pre-adjuster inspection.

Hassle-Free Insurance Claim Assistance in Tulsa

Dealing with the aftermath of an Oklahoma storm is stressful enough without the headache of insurance paperwork. You don’t have to navigate this complex system alone. Rescue Roofing Tulsa simplifies the entire journey for you, acting as your professional advocate from start to finish. We’ve spent years building a reputation as Tulsa’s most trusted roofer by providing clear, honest guidance to our neighbors.

Our team understands the specific challenges of the local climate. We know that a small leak today can lead to major structural issues tomorrow. By choosing a local, family-owned company, you’re getting a partner who is personally invested in the safety of your community. We handle the heavy lifting so you can focus on getting your life back to normal.

Why Choose Rescue Roofing Tulsa?

Quality matters when it comes to your home’s primary defense. We are proud to hold GAF Master Elite status. This is a prestigious certification that only 2% of roofing contractors in North America achieve. It means your roof replacement is backed by superior workmanship and the best warranties in the industry. We don’t just fix roofs; we provide long-term protection.

- Expertise in Prevention: We prioritize proactive roof maintenance to help you avoid frequent claims and extend the life of your shingles.

- Paperwork Assistance: Our staff helps you understand the technical jargon in your policy and assists with the documentation required by your provider.

- Durable Materials: We use high-quality products specifically tested to withstand the high winds and heavy hail common in Tulsa and surrounding areas.

Get Started with a Free Storm Damage Inspection

Understanding how to file a roof damage insurance claim starts with an accurate assessment of the damage. We offer a no-obligation roof inspection to give you the facts you need. During our visit, we’ll perform a comprehensive check of your roofing system, including shingles, gutters, and ventilation.

We provide a transparent report of our findings so you can make an informed decision. If we find storm damage, we’ll be there to meet with your insurance adjuster to ensure nothing is overlooked. This professional oversight helps ensure your claim is processed fairly and accurately. Don’t wait for a leak to appear before taking action. Schedule your free inspection with Rescue Roofing Tulsa today and experience a truly hassle-free restoration process.

Take the Stress Out of Your Tulsa Roof Recovery

Navigating the complexities of insurance coverage doesn’t have to be a burden. You now understand the critical differences between Actual Cash Value and Replacement Cost Value. You also know that meticulous preparation for the adjuster meeting is the best way to protect your home’s value. Knowing how to file a roof damage insurance claim is the first step toward getting your life back to normal after an Oklahoma storm. It’s about more than just repairs; it’s about restoring your peace of mind with a clear plan of action.

As a local family-owned and operated business, we treat every roof like it’s our own. T-Town Roofing brings the elite standard of a GAF Master Elite Certified Contractor to your doorstep, ensuring your home receives top-tier materials and expertise. We back our quality with a 10-year workmanship warranty so you stay protected long after the initial repairs are finished. We’re here to handle the paperwork and the heavy lifting for you so the entire process remains hassle-free.

Get Your Free Storm Damage Inspection & Claim Assistance

Your home deserves the best protection available in Tulsa. We’re ready to help you restore your roof and your confidence.

Frequently Asked Questions

How long do I have to file a roof insurance claim in Oklahoma?

You typically have 12 months from the date of the storm to file a claim in Oklahoma. While state law provides a general framework for insurance companies, most standard homeowner policies in Tulsa require action within one year. We recommend starting the process immediately after a storm to ensure you meet all deadlines. Waiting longer than 365 days often results in a denial of coverage for that specific weather event.

Will my insurance premiums go up if I file a claim for storm damage?

Filing a single claim for storm damage usually won’t cause your individual rates to rise. Insurance companies view hail and wind as “Acts of God,” which are events outside your control. However, premiums in the 74101 zip code and surrounding Tulsa areas often fluctuate based on regional weather patterns. If a major storm affects 30% of your neighborhood, rates might increase for everyone in that area regardless of who files a claim.

Can I choose my own roofing contractor for the repairs?

You have the legal right to choose any contractor you trust to repair your home. Your insurance company might suggest a preferred provider, but you aren’t required to use them. As a local family-owned business, we focus on providing honest assessments that prioritize your home’s safety. Choosing a GAF Master Elite contractor ensures your roof meets high industry standards that local adjusters recognize and respect during the inspection process.

What happens if the insurance estimate is lower than the contractor’s quote?

We often find that initial insurance estimates miss specific line items like local building codes or high-quality underlayment. If the estimate is lower than our quote, we provide the adjuster with a supplement request. This document includes photos and accurate measurements to explain why the additional funds are necessary. We handle this communication to ensure your claim covers the full cost of a durable, professional installation that protects your family.

Do I have to replace my roof if the insurance company pays the claim?

You should replace the roof promptly once the check is issued. Most mortgage lenders require repairs to protect their investment, and failing to do so can lead to a force-placed insurance policy. Additionally, if you don’t use the funds for the intended repair, your insurance company will likely exclude the roof from future coverage. They may even cancel your policy within 30 days of discovering the work wasn’t completed.

Is hail damage covered if it does not cause an immediate leak?

Hail damage is covered even if you don’t see water inside your home. Impact from hailstones as small as 1 inch can bruise the shingles and strip away protective granules. This damage shortens the lifespan of your roof by 5 to 10 years and leads to leaks later. Learning how to file a roof damage insurance claim early helps you address these hidden issues before they turn into expensive interior repairs or structural problems.

What is a “proof of loss” form and when do I need it?

A proof of loss is a formal legal document where you swear to the facts of your claim under oath. You typically need to submit this within 60 days of the insurance company’s request. It includes the date of the loss, the cause of damage, and the total cost of the repairs. Our team helps you gather the necessary documentation so this step remains a hassle-free part of your recovery process after a storm.

Can I file a claim for a roof that is more than 15 years old?

You can file a claim on an older roof, but the payout depends on your specific policy type. Many policies switch from Replacement Cost Value to Actual Cash Value once a roof passes the 15-year mark. This means the insurer subtracts depreciation based on the roof’s age. If your roof is 18 years old, you might receive a smaller payout, but it’s still worth investigating how to file a roof damage insurance claim to offset your costs.