What if the “free roof” offer left on your doorstep is actually an invitation to commit insurance fraud? In Tulsa, many homeowners feel overwhelmed when they realize their wind and hail deductible is a percentage of their home value rather than a flat fee. It’s natural to look for ways to lower that out-of-pocket cost. However, under Oklahoma House Bill 1940, it’s illegal for a contractor to waive or rebate your deductible. If you’re searching for how to get help with roofing insurance deductible payments, you need a strategy that protects your home and your legal standing.

We understand that a sudden multi-thousand dollar expense feels daunting. You deserve a partner who explains the process clearly and honestly. This guide will help you discover ethical ways to manage your deductible and navigate the complexities of RCV versus ACV payments. We’ll also show you how to identify common industry scams and take advantage of new 2026 consumer protections. By the end, you’ll know how to ensure your insurance company pays the full fair value for your claim while keeping your investment secure.

Key Takeaways

- Understand why Oklahoma deductibles are shifting from flat fees to percentage-based amounts and how this affects your repair budget.

- Explore legal, monthly payment strategies for how to get help with roofing insurance deductible costs without violating state law.

- Identify the warning signs of “storm chaser” scams that promise to cover your deductible but often result in insurance fraud or liens on your property.

- Learn how accurate claim scoping identifies missed damage, helping you receive the maximum fair payout from your insurance provider.

- Discover the benefits of partnering with a local expert who provides transparent insurance claim assistance and follows strict ethical standards.

What is a Roofing Insurance Deductible and Why is it So High?

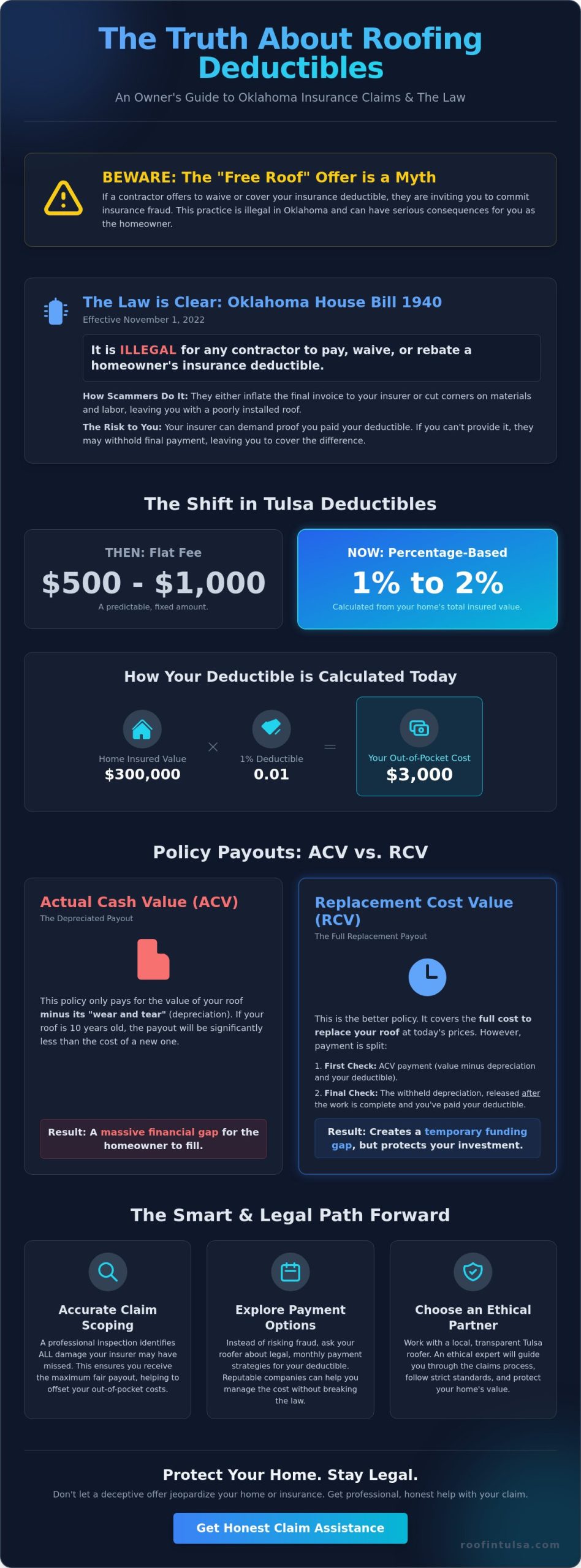

An insurance deductible is the specific amount you agree to pay toward a loss before your insurance provider begins to cover the remaining costs. For a foundational look at this concept, you can read more about What is a Roofing Insurance Deductible and how it functions as a risk-sharing tool between you and your carrier. In Tulsa, this number has changed significantly over the last few years. While many homeowners remember a time when a standard $500 or $1,000 flat deductible was the norm, those days are largely gone in Oklahoma.

Because our region faces some of the highest hail and wind risks in the nation, insurance carriers have shifted toward percentage-based deductibles to manage their exposure. This allows them to keep premiums from skyrocketing even further in a high-risk state. You can find your specific amount by looking at your policy’s “Declarations Page,” which is usually the first page of your insurance packet. It’s the summary that lists your coverage limits and the exact out-of-pocket requirements for different types of claims.

Flat vs. Percentage Deductibles in Tulsa

The biggest surprise for many local homeowners is the math behind a percentage-based deductible. If your policy has a percentage requirement, your out-of-pocket cost is tied to your home’s total insured value, not the cost of the roof repair itself. For example, if your home is insured for $300,000 and you have a 1% wind and hail deductible, you’ll be responsible for $3,000. If that deductible is 2%, your cost jumps to $6,000.

It is also vital to check if you have a separate “Wind and Hail” deductible versus an “All Perils” deductible. In Oklahoma, carriers often set the wind and hail portion much higher because storm damage is so frequent. Understanding these numbers is the first step in learning how to get help with roofing insurance deductible costs legally and effectively. These percentage-based models are quickly becoming the standard for almost every major carrier in the Tulsa metro area.

ACV vs. RCV: How it Impacts Your Initial Payment

The type of policy you hold, either Actual Cash Value (ACV) or Replacement Cost Value (RCV), dictates the size of your first claim check. ACV policies only pay for the depreciated value of your roof based on its age. If your shingles are ten years old, the insurance company subtracts that “wear and tear” from your payout. This often leaves a massive financial hole for the homeowner to fill.

RCV policies are generally more protective. They cover the full cost to replace the roof at today’s market prices. However, even with an RCV policy, the insurance company typically withholds the depreciation amount until the work is finished and they receive a final invoice. This creates a temporary funding gap. Homeowners often feel stuck during this period, wondering how to get help with roofing insurance deductible expenses when the initial check doesn’t cover the full materials and labor required for a quality installation.

Can a Roofer Waive My Deductible? (The Legal Truth)

In Oklahoma, the law is very clear on this matter. As of the current 2026 legal landscape, it is illegal for roofing contractors to waive, pay for, or rebate a homeowner’s insurance deductible. This requirement is strictly enforced under Oklahoma House Bill 1940, which took effect on November 1, 2022. When a contractor offers to “absorb” your deductible, they are asking you to participate in a scheme that violates state law. If you are looking for how to get help with roofing insurance deductible costs, it is vital to stay within legal boundaries to protect your home and your future coverage.

These “waiving” schemes usually rely on two dishonest methods. First, the contractor might inflate the invoice sent to your insurance company to cover the cost of the deductible. Second, they might cut corners on materials and labor to save money, leaving you with a subpar roof that may fail during the next storm cycle. Insurance companies are well aware of these tactics. They often demand proof of payment, such as a canceled check or bank statement, before releasing the final replacement cost value check. If you cannot prove you paid your deductible out of pocket, the insurer may withhold those funds indefinitely.

Trust is the foundation of any professional relationship. If a roofer is willing to misrepresent facts to an insurance company, they are likely to be just as dishonest with you. A contractor who breaks the law to get your business will probably not be around to honor warranty promises if your roof leaks a year from now. For a deeper understanding of what insurance fraud is, you can review the standards set by the National Association of Insurance Commissioners. It is always better to work with an ethical partner who prioritizes your long term security.

Common ‘Deductible Assistance’ Scams to Avoid

Watch out for these red flags when door to door “storm chasers” knock on your door after a Tulsa hailstorm:

- The “Free Roof” Pitch: Any claim that you won’t have to pay a dime out of pocket is a major warning sign of fraud.

- Rebates or Advertising Credits: Some roofers offer “sign credits” in exchange for placing a sign in your yard. If these credits exactly match your deductible amount, it is a transparent attempt to bypass the law.

- Inflated Estimates: If a roofer suggests submitting a higher price to the insurance company than what they actually plan to charge you, they are committing fraud.

These “deals” often lead to disaster. If an insurance company denies an inflated claim or discovers the fraud, the contractor may place a lien on your property to recover their costs. Before signing any contracts, it is wise to get a professional roof inspection from a local team that follows the letter of the law.

The Consequences of Deductible Fraud

Participating in these schemes carries heavy risks for homeowners. You could face the immediate loss of your insurance coverage or a total policy cancellation. In Oklahoma, both the contractor and the homeowner can face legal repercussions for these actions. Deductible fraud is the intentional misrepresentation of repair costs to an insurer. It is simply not worth the risk of legal trouble or losing the protection of your home insurance policy. Instead, focus on legal ways to manage your out of pocket expenses while ensuring your roof is built to last.

Legal Ways to Get Help With Your Roofing Deductible

Finding the money for a high deductible is often the most stressful part of the storm recovery process. Since waiving the deductible is illegal in Oklahoma, you need a realistic plan to cover the cost without draining your emergency savings. Many Tulsa homeowners find that flexible financing is the most manageable path forward. By spreading the cost over several years, a $3,000 deductible can be broken down into affordable payments as low as $50 per month. This allows you to secure your home immediately while keeping your monthly budget intact. If you are struggling to find how to get help with roofing insurance deductible payments, specialized financing is often the most reliable answer.

Another option is a Home Equity Line of Credit (HELOC). If you have built up equity in your Tulsa property, a HELOC often provides lower interest rates than standard credit cards. It functions like a revolving credit line that you can use specifically for emergency property repairs. Personal loans designed for home improvement are also widely available. These are typically unsecured loans with fixed rates and set repayment terms. They offer a straightforward way to bridge the financial gap between your initial insurance check and the final cost of the project. Working with local contractors on a structured payment schedule can also help you manage the timing of these out of pocket expenses.

Roofing Financing: Making the Deductible Affordable

Traditional bank loans can be slow and require significant paperwork. Specialized roofing lenders are different because they understand the urgency of storm damage. Many offer “No Interest and No Payment” introductory periods. This is particularly helpful if you are waiting for your insurance company to release your final replacement cost check. You can explore Rescue Roofing Tulsa’s financing options to see which programs might fit your specific situation. Being proactive about your budget helps you avoid the pressure of common roofing scams that promise “free” services but deliver legal headaches.

Government and Non-Profit Assistance Programs

For those who qualify, local community grants can provide a vital lifeline. In Tulsa, there are often specific programs aimed at helping low income seniors or veterans with essential home repairs. If a storm is part of a federally declared disaster, SBA Disaster Loans may also become available. These low interest loans can sometimes be used to cover insurance deductibles when other funding isn’t available. Learning how to get help with roofing insurance deductible costs through legal channels ensures your claim remains valid. Regarding tax implications, you should consult with a CPA about casualty loss deductions. While tax laws are complex, these deductions can sometimes offer relief if your losses from a storm exceed a specific percentage of your adjusted gross income.

How Claim Assistance Reduces Your Out-of-Pocket Burden

While you cannot legally avoid your deductible, you can certainly ensure that you aren’t paying for repairs that your insurance policy should already cover. Many homeowners assume the initial estimate from an insurance adjuster is the final word on the project’s cost. This is rarely the case. Insurance adjusters are often handling dozens of claims after a major Tulsa storm. They might miss critical details or local building code requirements that are essential for a safe, long-lasting roof. This is where professional insurance claim assistance becomes your greatest asset. By having an expert contractor present during the inspection, you ensure the scope of work is accurate from day one.

If you’re wondering how to get help with roofing insurance deductible burdens, the answer often lies in accurate scoping. When a contractor identifies items the adjuster missed, those costs are added to the claim rather than coming out of your pocket. This prevents you from paying for “extras” that are actually standard requirements for a professional installation. A skilled contractor speaks the same technical language as the insurance company. They provide the documentation, photos, and local code references needed to justify the full cost of the project. This collaborative approach ensures the insurance company pays the full fair value for the damage; it leaves you responsible only for your legally required deductible.

Ensuring an Accurate Scope of Work

It’s common for initial adjustments to miss code-required components like drip edges, starter shingles, or ice and water shields. In Tulsa, these aren’t just recommendations. They are necessary for a roof to meet current safety standards. Documenting every flashing detail and shingle condition ensures the insurer covers the real cost of materials and labor. It’s also helpful to stay current on roofing maintenance throughout the year. Regular upkeep provides a clear record of your roof’s condition. This makes it much harder for an insurance carrier to deny coverage based on “pre-existing wear and tear” when a storm finally hits.

The Supplement Process Explained

Sometimes, the true extent of the damage isn’t visible until the old shingles are removed. If a roofer discovers rotted decking or compromised structural elements during the tear-off, they must pause and document these findings. This triggers the “Supplement” process. Supplementing the claim allows the contractor to submit additional evidence to the insurance company for items that weren’t in the original estimate. This ensures the insurer covers the true cost of the roof repair without the homeowner being forced to pay for unforeseen complications. This process is the most effective legal way to minimize your financial stress. If you need help managing a complex claim, reach out to our team at Rescue Roofing Tulsa for professional guidance.

Navigating Your Tulsa Roof Claim with Rescue Roofing Tulsa

At Rescue Roofing Tulsa, we believe the insurance process shouldn’t feel like a second job for you. Our team is deeply committed to providing ethical, legal, and transparent insurance claim assistance. We don’t just replace shingles; we act as a trusted advisor for our neighbors. Before a single shingle is removed, we take the time to help you understand your specific policy. This clarity ensures you aren’t surprised by costs halfway through the project. If you’re wondering how to get help with roofing insurance deductible payments, the most reliable path is through a partner who knows Oklahoma law and Tulsa’s unique climate.

Local roots matter when it comes to your home’s protection. National “storm chasers” often leave the state once the storm season ends, making it nearly impossible to get warranty support later. Because we are a Tulsa-based company, Rescue Roofing Tulsa is here for the long haul. We stand by our work and our community. Our process is methodical and unhurried. We guide you from the initial inspection through the final insurance documentation. This steady approach builds the confidence you need to manage a stressful situation with ease.

Transparent Estimates vs. ‘Storm Chaser’ Promises

We provide detailed, line-item estimates using Xactimate, which is the same industry-standard software used by insurance adjusters. This creates a common language between our team and your insurance carrier. It helps prevent the “scoping gaps” that often lead to out of pocket expenses for homeowners. Our philosophy is simple: we treat every roof like it’s our neighbor’s. This commitment to quality extends beyond homes; we also provide expert commercial roofing in Tulsa for local business owners. Whether your property is large or small, you deserve an honest assessment and a fair price.

Ready to Start Your Claim?

The first step toward a secure home is a professional assessment. You can schedule a no-obligation roof inspection to determine the true extent of your storm damage. When you meet with your insurance agent, it’s helpful to have a few items ready. Keep your policy declarations page, your claim number, and any initial adjuster reports handy. We can review these documents with you to identify how to get help with roofing insurance deductible financing or to spot missed items in the original scope. Our goal is to remove the administrative burden from your shoulders so you can focus on getting your life back to normal. If you’re ready for a partner you can trust, Contact Rescue Roofing Tulsa for Insurance Claim Assistance today.

Secure Your Home with Confidence

Navigating a storm claim doesn’t have to be a source of constant anxiety. You now know that while waiving a deductible is illegal in Oklahoma, there are many ethical ways to manage the cost. By choosing flexible financing and ensuring your claim is fully supplemented for code-required items, you protect both your home and your legal standing. Understanding how to get help with roofing insurance deductible payments is really about finding a partner who prioritizes your long term security over a “quick fix” sales pitch.

As an A+ rated local Tulsa contractor, Rescue Roofing is here to serve as your advocate. We use our deep expertise in Xactimate and insurance supplementing to make sure no damage is overlooked by your adjuster. If the upfront cost is a concern, we also offer flexible financing plans to fit your monthly budget. Get Professional Insurance Claim Assistance from Rescue Roofing Tulsa today to start your recovery. You’ve worked hard for your home. We’re ready to help you protect it with the honesty and quality you deserve.

Frequently Asked Questions

Is it illegal for a roofer to pay my deductible in Oklahoma?

Yes, it is strictly illegal under Oklahoma law for a contractor to pay, waive, or rebate your insurance deductible. This regulation is designed to prevent insurance fraud and protect the integrity of the claims process. Both the contractor and the homeowner can face legal consequences for participating in such a scheme. It is always best to work with an ethical professional who follows state laws to ensure your claim remains valid.

What happens if I can’t afford my roofing deductible?

If you lack the immediate cash to cover your out of pocket portion, you should explore legal financing options or personal loans. Many local contractors partner with specialized lenders to offer monthly payment plans that make the expense much more manageable. You might also consider a home equity line of credit or community grants if you qualify. Learning how to get help with roofing insurance deductible costs through these official channels protects your financial future.

Can I use my own materials to save on the deductible cost?

Most professional roofing companies do not allow homeowners to provide their own materials for insurance funded projects. This is because the contractor cannot guarantee the quality or provide a long term warranty for materials they did not source themselves. Additionally, insurance payouts are based on specific material grades. Using cheaper, self sourced materials to save money could be viewed as a misrepresentation of the actual repair costs to your insurance provider.

Why did my insurance company only send me a check for half of the roof cost?

This is common if you have a Replacement Cost Value policy that includes recoverable depreciation. The first check usually covers the Actual Cash Value, which is the depreciated value of your old roof minus your deductible. The remaining funds are typically held back until the work is finished and a final invoice is submitted. This process ensures that the repairs are performed according to the agreed upon scope before the full payout is released.

Do I have to pay my deductible upfront to the roofing company?

Payment timelines vary by contractor, but the deductible is your legal responsibility as the first part of the project’s funding. Some companies require the deductible amount as a deposit to order materials and schedule the crew. Others may collect it upon the completion of the job. You should always clarify the payment schedule in your written contract to ensure there is no confusion about when your out of pocket portion is due.

Can I negotiate my deductible with my insurance company?

You cannot negotiate the deductible amount after a storm occurs because it is a fixed part of your legal contract with the insurer. The deductible was chosen when you first signed or renewed your policy. While you can’t change it for an active claim, you can review your policy annually to adjust your deductible for future events. Increasing your deductible can lower your monthly premiums, but it also increases your financial risk during a claim.

How do I know if a roofer is trying to involve me in insurance fraud?

A major red flag is any offer to “waive” or “cover” your deductible in exchange for your business. If a roofer suggests submitting an invoice to the insurance company that is higher than what they actually plan to charge you, that is fraud. Ethical contractors provide transparent, line item estimates. They will never ask you to hide information or misrepresent the true cost of repairs to your insurance carrier.

Can I get a loan just for my insurance deductible?

Yes, many homeowners secure personal loans or specialized home improvement financing specifically to cover their deductible. This is a common strategy for those looking for how to get help with roofing insurance deductible payments without depleting their savings. These loans often have fixed interest rates and predictable monthly payments. Using a legal loan ensures that you fulfill your contractual obligation while getting your roof replaced immediately by a professional team.